2021 again saw a booming property market in Istanbul. Pent up demand coupled with drastically low supply of new property, saw a surge in prices. So what exactly happened in 2021, and what can we expect to see in 2022?

Pandemic fuels demand for terraced apartments

Lockdowns affected all countries across the world and Istanbul was no exception. People craved outdoor spaces – the vast majority of apartment buildings in Istanbul don’t have any garden space, and parks are few and far between. Compounds with large garden space and apartments with balconies/terraces saw huge demand. Villa prices surged as people craved outdoor spaces.

Central bank interest rates

The governments insistence on reducing interest rates despite rising inflation continued the buying cycle. With other assets losing value, investors turned to real estate and cars as a hedge against rising assets prices.

January 2021 – low stock levels

In 2020, stock levels of brand new property were reduced even further. 2021 was no exception. With uncertainty surrounding the pandemic, and rising costs, developers were hesitant to start new projects. Central Istanbul locations have a drastic problem with a supply of earthquake proof, quality apartments.

Heavy internal demand

International buyers only make up a small proportion of investors in Istanbul. The vast majority of investors are within Turkey and expats Turks. This external demand on Istanbul is fuelled by a desire of Turks to have a piece of Istanbul. This issue is now even pushing out local Istanbullites, with the majority of youngsters now coming on to the property ladder not able to afford property in Istanbul. A recent survey showed that in 2019, nearly 60% of local Istanbul residents could afford to buy a property in Istanbul – in early 2022, this number fell to 25%.

What we expect in 2021

With record high prices, we now expect developers to take the plunge and start building again. Unfortunately this will not help prices in the city centre as there is very little land. The majority of this building of large compounds will be on old factory and warehouses in regions like Kagithane, Media Highway, and on the Anatolian side, in Maltepe and Kartal.

City centre – Sisli and Besiktas

The traditional “central” parts of Istanbul, Sisli, Besiktas, Kadikoy, Bakirkoy, and Zeytinburnu, suffer from undersupply of brand new property. This chronic undersupply will continue into 2022 and beyond. “New” high rise permits in Sisli are now impossible to come by, whilst in Besiktas, Zeytinburnu and Bakirkoy, high rise permits were never given beyond 15 stories.

The Greater Istanbul Municipality (IBB), coupled with the Turkish government, prefer “horizontal” architecture as a solution to the overly dense nature of today’s Turkish neighbourhoods. Expect to see smaller boutique “regeneration” projects in these regions.

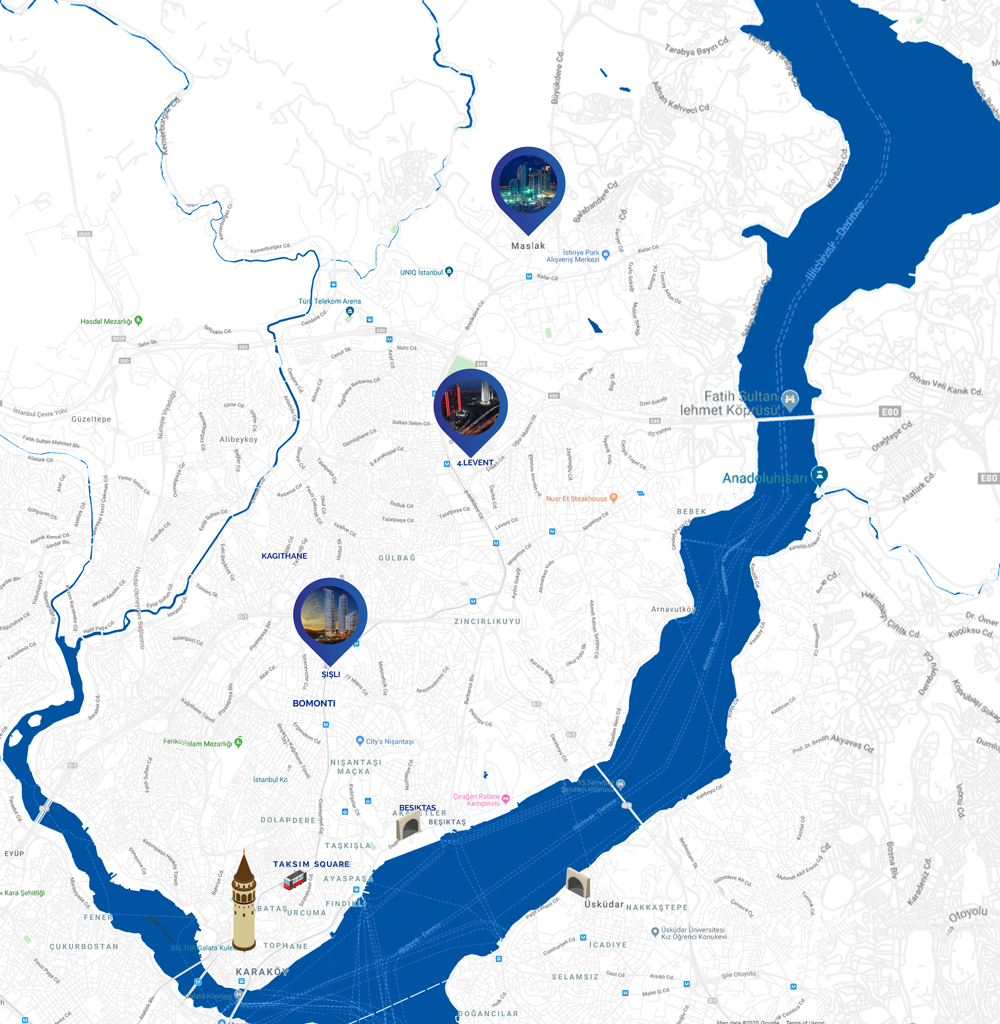

Istanbul’s premier business district starts in Sisli (pronounced Shishli) and extends North to Mecidiyekoy, Levent, 4. Levent and ending in Maslak. Sisli is prime city centre and in exceptionally high demand for residential and commercial space. Development in this region is rare and usually quite expensive as vacant land no longer exists.

Bomonti is a region which was a ghetto just five years ago. Today, it is an elite residential region, with skyscrapers like Anthill, Divan, and Bomonti Hilton (the largest Hilton in Europe). The residential towers average in excess of $6,000 per square metre.

Bomonti’s popularity gained with the construction of two road tunnels, one which leads directly to Besiktas, and the other leads up to Kagithane. Two very important tunnels. In addition, Taksim is 9 minutes away, Nisantasi (a very elite area) is a 10 minute walk away, the Taksim metro (M2) is a five minute walk. Bomonti today is an important, yet still growing region.

Kagithane – Seyrantepe – Istanbul’s rapidly expanding technology district

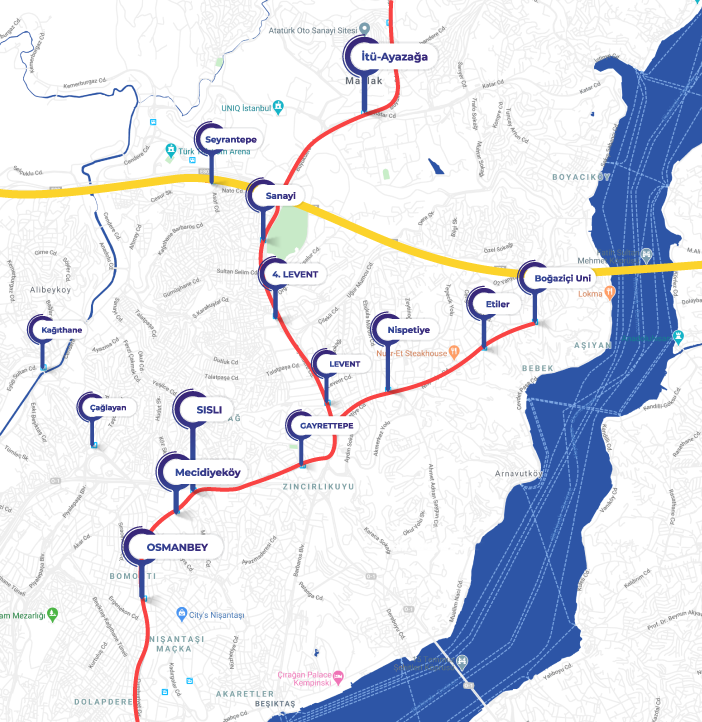

Whilst most people know Seyrantepe due to the famous Vadi Istanbul mall, most people are not aware of it being called Seyrantepe. International buyers are miscommonly told this region to be Maslak or the Vadi district. These two zones are gradually merging, along the Cenderre river banks. Starting in Seyrantepe, incredible developments have cropped up along the river, working its way south towards the Halic river. Whilst prices have topped out in Seyrantepe, moving further south offers an opportunity for real value.

While the new M7 metro line opened in Q4 2020, the pace of development has quickened now that the potential of the new line is realised. The M7 metro line runs east from this region into the city centre at Sisli, and terminates at the Bosphorous in Besiktas. This line is of crucial importance to Istanbul as it will be the first East to West metro line link for the city centre.

The new Airport is also easy to access from this region, with a direct highway link from Kagithane to the airport – the D020. The airport is to be served by a metro line due to open next year, and with a station in Kagithane (M11 Gayrettepe – Istanbul Airport metro line).

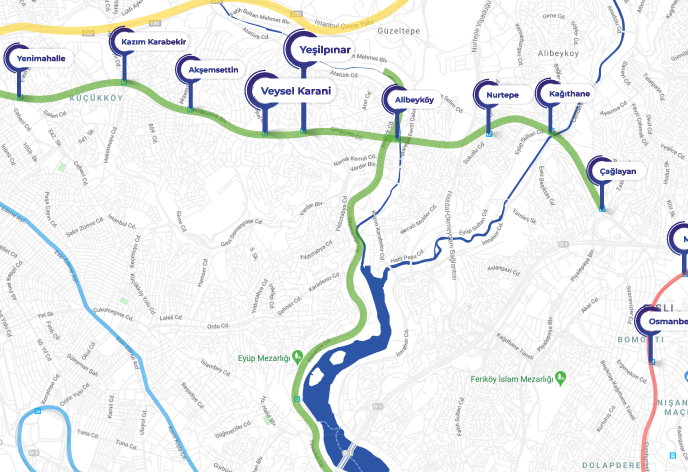

Expect Kagithane to perform high double digit growth throughout 2021 in areas outside of the prime regions – i.e. urban regenaration areas outside the Vadi Istanbul mall region.

Kemerburgaz and Gokturk

These two small “villages” are traditionally for the wealthy upper classes of Istanbul. However, the new M11 airport metro lines opens in Q4 2022, linking the region directly to Zorlu within 15 minutes – basically the city centre. This offers a huge opportunity for investors as the region is currently undervalued. One beds can be found for c$200,000 as of Jan 2022, and this is genuinely unique – no other parts of Istanbul can offer this prices and still be within 10-15 minutes of the city centre. Read more about these regions on our blog here- Gokturk and Kemerburgaz, what’s the fuss?

GOP and Eyup

Regions which line central districts are expected to pick up the slack of the city centre. Regions like Eyup and Gaziosmanpasa provide easy access to city centre locations. Government expenditure on metro lines, the most recent being the M7 metro and T5 tramline, has seen even more private investment in these areas. These districts have plenty of space for further construction. Couple this with extremely unsafe stock under “urban regeneration” orders, and a decent supply of mid range property will continue to feed the market.

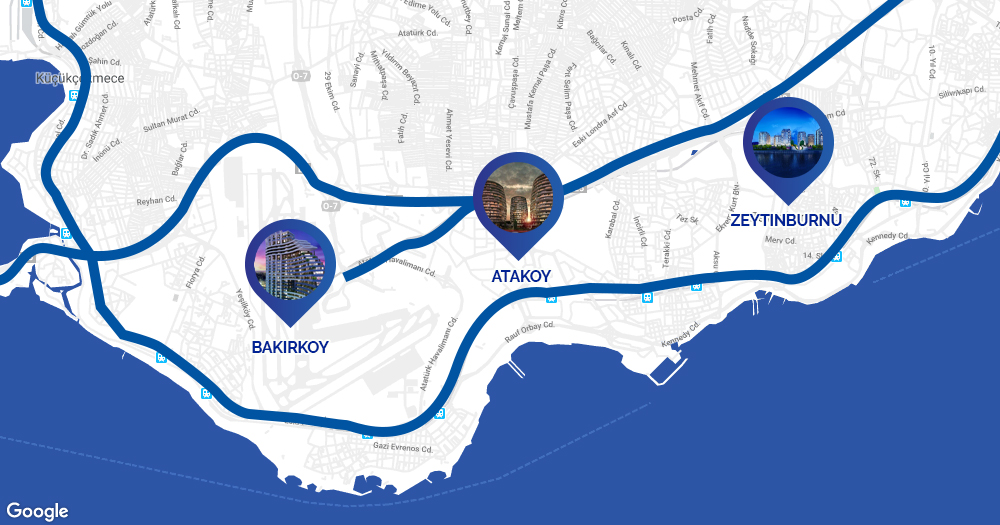

Coastal route – Atakoy, Bakirkoy, and Zeytinburnu

The coastal route provides enticing sea views as well as excellent transport links to all parts of Istanbul. The region also provides a fantastic lifestyle to residents with excellent and varied amenities of all kinds. These regions are prime for the upper and middle classes.

The front line has seen heavy development of mega compounds – these are without doubts future landmarks of Istanbul. These provide full uninterrupted sea views across the Marmara sea, the Prince’s islands, and across the historic peninsula. They are once in a generation developments, with no further land remaining for compounds of these kinds.

The uber modern Marmaray train line provides high speed access to all parts of Istanbul, and runs without interruption under the Bosphorous, the Anatolian side, and all the way to Ankara as a high speed trainline. This has made these regions even more attractive to frustrated commuters.

Despite being in the upper bracket in terms of price, these developments are prime for investment. They will be easy to rent, and with strong demand from the local and international market, the resale value will always be there. Supply however is quickly running out as most compounds have completed, and are more attractive to the end user. Further supply and permits will be extremely hard to come by, resulting in strong capital gain in 2022.

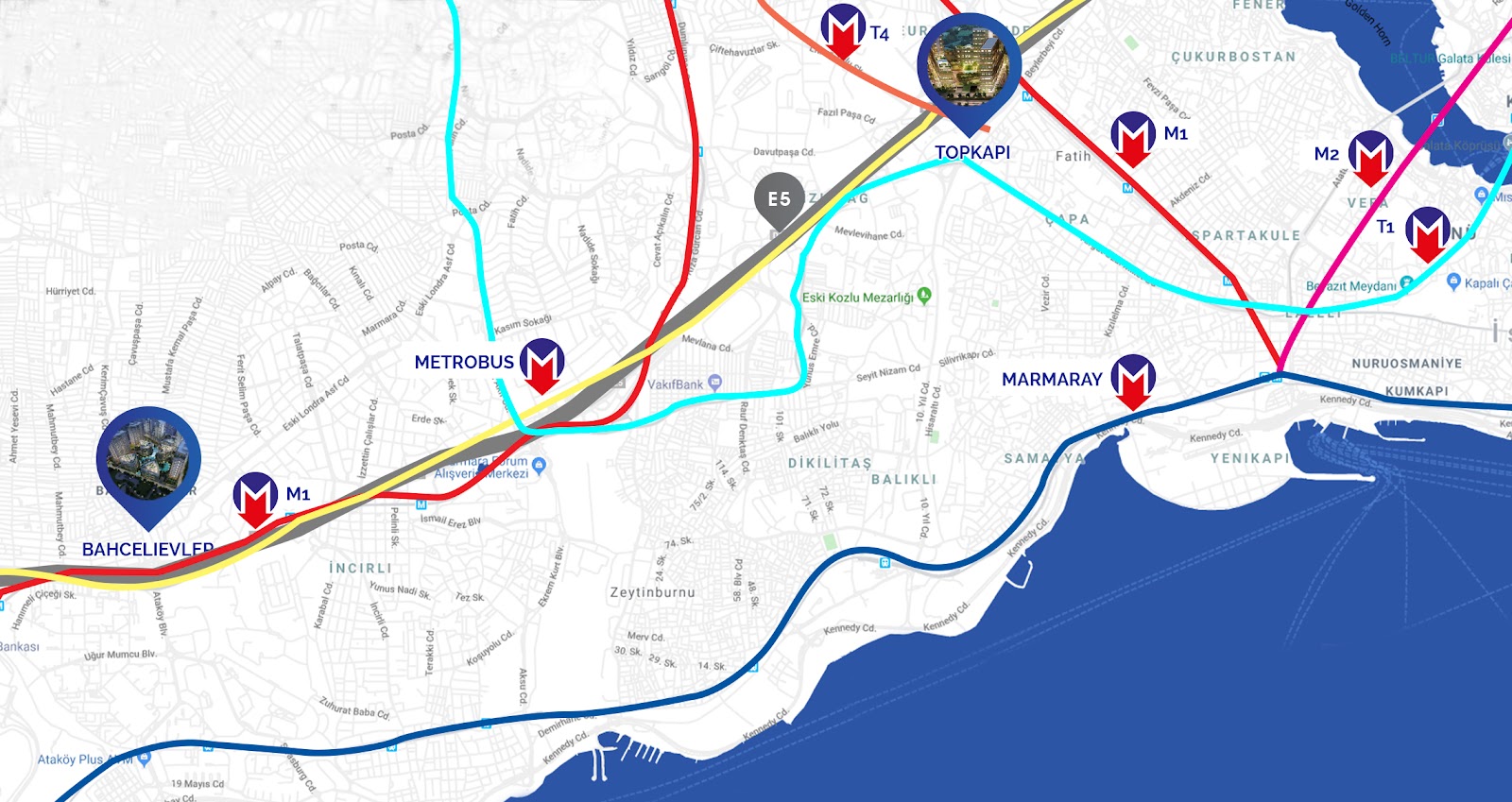

The crossroads of Istanbul – Bahcelievler and Topkapi

These regions are always attractive to the middle classes of Istanbul. Providing easy access to the E5 means multiple transport options to all parts of the city, but most importantly to the city centre and business district. The region is traditionally heavily dense, with narrow streets, and lack of underground parking the main issues.

This changed over the last five years, with old warehouses and factories moving to the suburbs of Istanbul, large compounds have replaced them. This has driven growth in the area, with prices remaining reasonable considering the location.

The region is quite mature, and no new government investment is expected until before 2023 – hence prices remained stagnant in 2021 and indeed may for 2022. Good capital gain can be made in off plan projects.

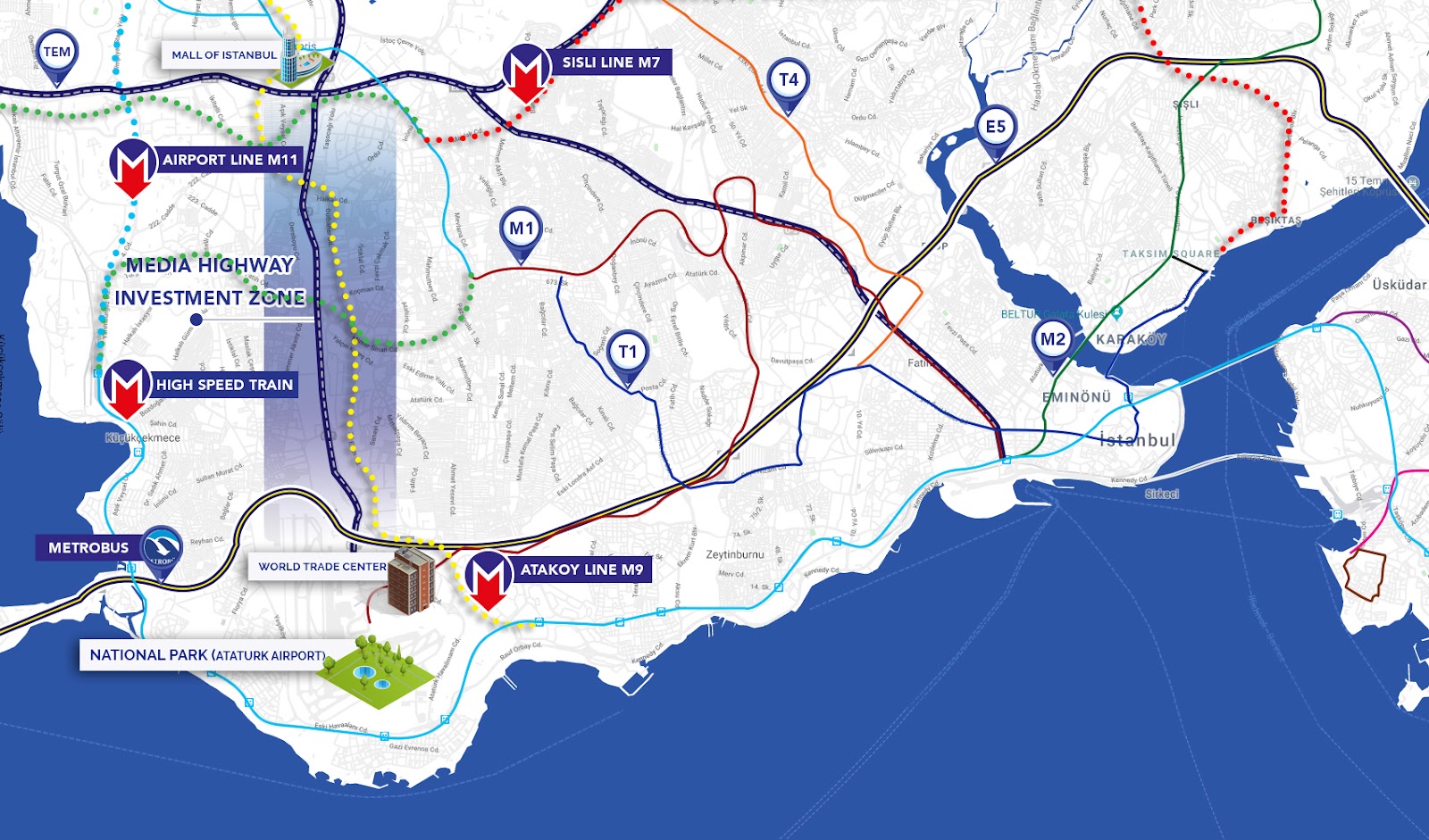

Media Highway and Atakent

Moving further west, “Media Highway” (Basin expres), continues its regenaration apace. Three metro lines, one which opened in 2020 (M7), continues to fuel heavy construction around metro stations. This planned government expenditure on rail lines is a welcome respite from the older planning of build the homes first and then the infrastructure. An approach which has caused Istanbul’s infamous traffic issues. Today, Media Highway provides ample stock – but expect this stock to dwindle once the M9 and M3 metro lines open. Both are expected in Q4 2022.

Key facts about this crucial region:

Atakent and Halkali in Kucukcekmece has always been a safe haven for the middle classes. Its rapid expansion throughout the 2010s out of Atakoy has transformed rocky land into a paradise of compounds, private schools and hospitals, many malls, and excellent infrastructure. Today, Halkali is the terminal for the country’s national and international high speed train network, as well as Marmaray, M1a metro, and the new Istanbul airport M11 metro line. This is further fuelling demand for what is a prime example of what proper town planning can do in Istanbul.

We expect exceptional growth in price rises in property that is located within 800 metres of a metro station – especially Halkali.

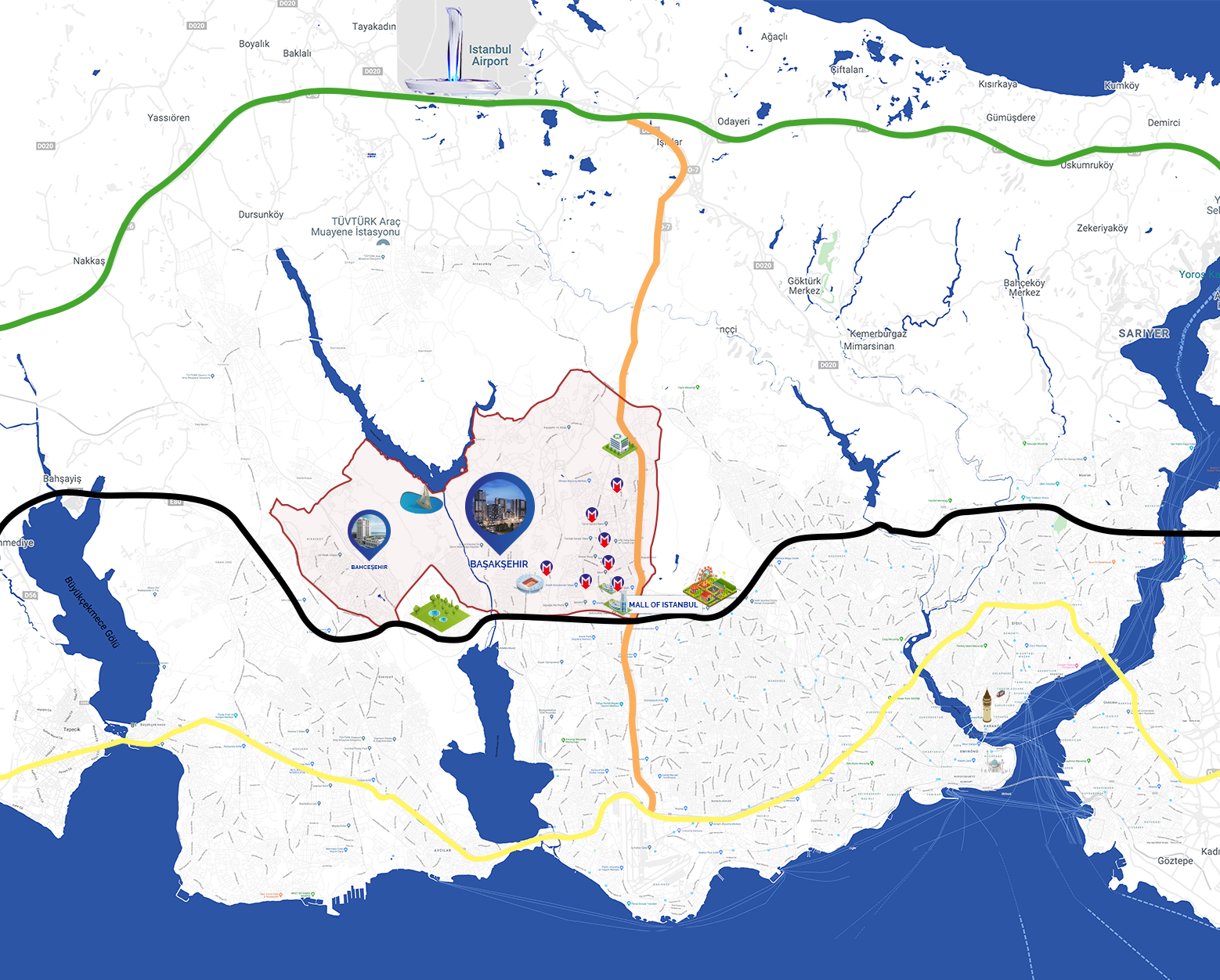

Basaksehir and Bahcesehir

These two regions are investor favourites, but the important attributes of location, early phase of construction, and brand name builder, are very important here. This combination ensures resales are always fast, for a quick exit route no matter what the market conditions. The cheaper options will never provide a decent return, and resales take traditionally longer in my experience. In recent research, we found that return on investment levels reached 30 years, making it much more logical to rent in the region then buy.

Basaksehir and Bahcesehir are the closest satellite towns to the new airport, with a government objective of growing both into a population of one million plus. Parallel to this plan is to grow it with a master-plan – hence the broken thinking of the past of building first, bringing infrastructure later, is not in place here. Basaksehir is home to one of Istanbul’s biggest malls (Mall of Istanbul) and Istanbul’s biggest state hospital (3,000 beds). The metro linking the region to the city centre is already operational with construction for expansion already having started. Bahcesehir also has a metro construction linking it to the city centre at Sisli. These are all large scale public and private investments adding up to billions of dollars.

Esenyurt – A classic case of oversupply

Esenyurt continues with the classic case of oversupply in an area that does have healthy demand for budget real estate. Esenyurt is a clutter of skyscrapers, giving it an impressive skyline. However the district is a target for low demographics and has a large international population. Resale has traditionally been difficult here due to the combination of these reasons. Rental return is also exceptionally low, averaging 2-3%.

The serviced apartment and branded complexes are the safest concept in this region. This is where a management team will be within the complex, and this is generally available on projects built by major developers. The smaller developer does not have the experience or know how to provide this type of service – this does not mean small development, but the type of developer that set up fairly recently and would not have the knowhow.

Beylikduzu – An idyllic western town of Istanbul

Beylikduzu is an exceptionally large district made up of the southern portion of the E5 between the two lakes of Istanbul. This gives it a huge coastal line, making it a family holiday home favourite. In fact, traditionally the coastal lines has been a holiday home destination for middle class Turks since the 90s.

Much of the rise in Beylikduzu has been driven by “branded” projects in Yakuplu and Beykent. Standard buildings have not seen the same rises. Beykent has heavy demand both internationally and locally, with its private schools, malls, and private hospitals. Its proximity to the E5 make it an important satellite town for commuters, who rely on the metrobus system to get to the city centre fast. Due to height restrictions, a well controlled level of supply exists, and we are expecting to see good gains in 2022.

Yakuplu is situated on the coast and has boomed due to the ever expanding and popular West Istanbul Marina. The region may suffer from the fact that there is plenty of empty land for continued development, causing an oversupply in a region that is traditionally for holiday makers.

Buyukcekmece – a retirement and villa town

Buyukcekmece is the penultimate district in West Istanbul. Whilst the district does have a busy and congested town centre, much of the region is made up of holiday homes and villas. Holiday homes are centred around the coast line neighbourhood of Mimaroba. New secure compounds have lined this coast, providing access to sandy beaches and incredible views across the sea of Marmara and the Buyukcekmece lake. Due to the heavy restrictions on construction in this area (in terms of height and density), supply has not met demand.

Villas are expensive in all parts of Buyukcekmece, but especially so in Buyukcekmece. Much of the villas are set back in the north, in the Alkent neighbourhood. These villas have seen an average of 54% price rise, an incredible return for what are already expensive prices.